What Actually Happens When You Send Money Through UPI?

UPI made digital payments in India feel instant and effortless. This blog explores what actually happens behind a UPI transaction, how the technology works, why it became massive, and the hidden systems powering modern digital payments.

The hidden technology powering India’s instant payment revolution

Introduction: Sending Money Became Almost Invisible

A few years ago, sending money digitally in India often felt frustrating.

You had to:

- remember account numbers

- enter IFSC codes

- wait for bank processing

- sometimes deal with failed transfers

And depending on the system:

- payments could take hours

- bank timing mattered

- weekends caused delays

Now?

People casually send money in seconds while

- buying tea

- paying rent

- ordering food

- shopping online

- splitting dinner bills

Open app.

Scan QR.

Enter amount.

Done.

The transaction feels almost instant.

So naturally, a bigger question appears:

What actually happens behind the scenes when you send money through UPI?

Because despite feeling simple on the surface, UPI is one of the most sophisticated digital payment systems ever built at scale.

And in many ways, it completely changed how India interacts with money.

UPI Quietly Changed Everyday Life

Most technological revolutions feel dramatic.

UPI didn’t.

It arrived quietly.

Slowly.

Then suddenly everyone was using it.

Street vendors.

Small shops.

Large companies.

Food stalls.

Taxi drivers.

Shopping malls.

Online stores.

QR codes became part of everyday India.

And that’s what makes UPI fascinating.

It didn’t just modernize banking.

It changed behavior.

Before UPI: Digital Payments Were Complicated

To understand why UPI became massive, we first need to understand the problems it solved.

Before UPI, digital banking often depended on systems like the following:

- NEFT

- RTGS

- IMPS

These systems worked.

But they weren’t designed for the kind of instant, everyday payments people expect now.

The Problems With Older Banking Systems

Traditional transfers often involved:

- complicated setup

- bank account details

- waiting periods

- timing restrictions

- confusing interfaces

For small daily payments, this felt excessive.

Imagine buying coffee and needing:

- account number

- IFSC code

- transfer setup

That friction slowed adoption.

UPI changed that completely.

What Is UPI?

UPI stands for:

Unified Payments Interface

It was developed by National Payments Corporation of India (NPCI).

The goal was ambitious:

Create a system where:

- money transfers happen instantly

- banks communicate seamlessly

- users don’t need complicated banking details

- payments work 24/7

And somehow, it worked at a national scale.

The Biggest Innovation Was Simplicity

UPI simplified payments dramatically.

Instead of remembering:

- account numbers

- IFSC codes

Users could simply use:

- phone numbers

- QR codes

- UPI IDs

That sounds small.

But reducing friction changes adoption massively.

The Magic of the QR Code

One of the smartest parts of UPI was QR-based payments.

Why?

Because QR codes removed typing completely.

Instead of entering:

- account information

- payment details

Users simply scan and pay.

That simplicity accelerated adoption everywhere.

Especially among small businesses.

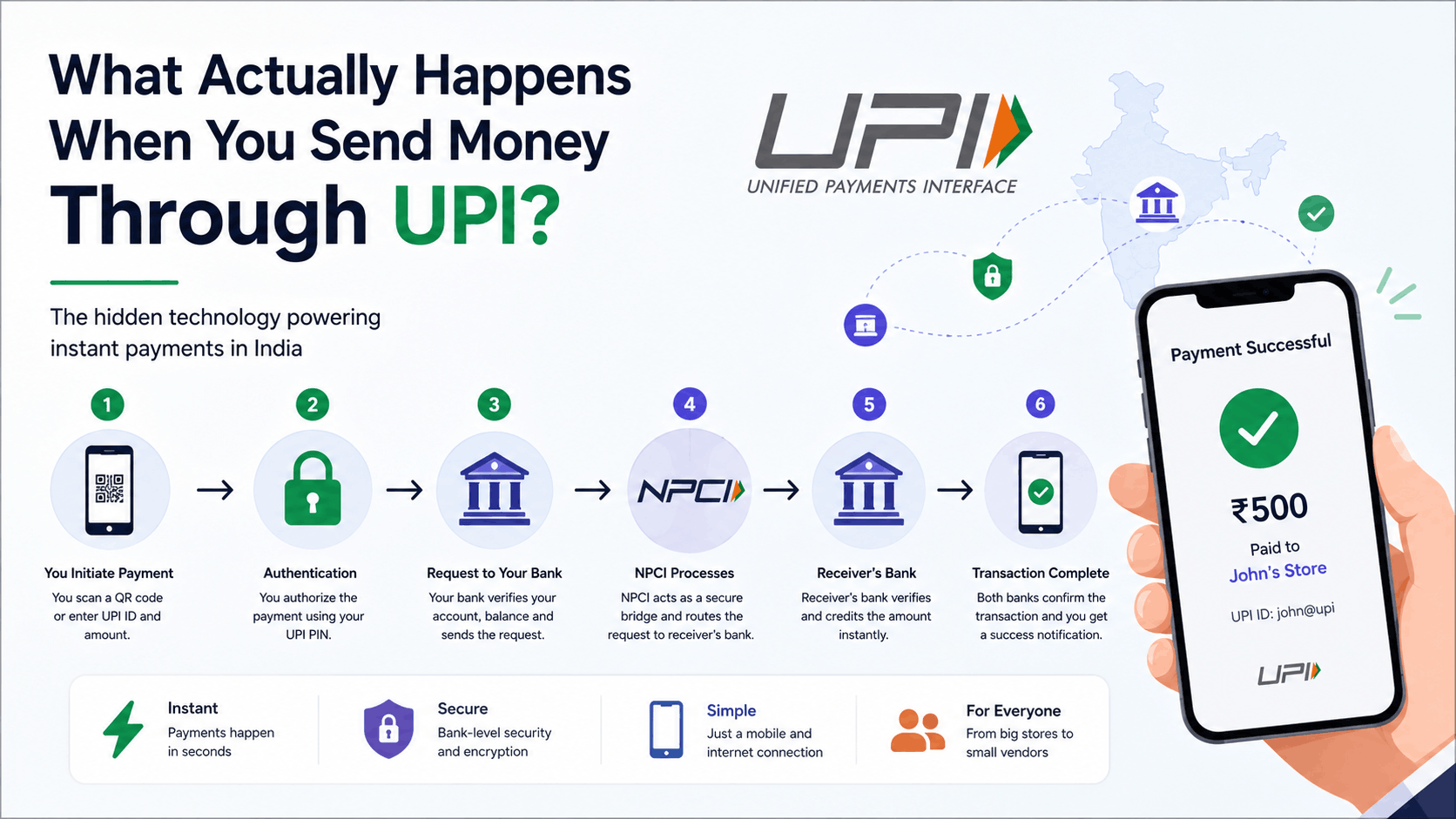

So What Actually Happens During a UPI Payment?

Now comes the interesting part.

Let’s break down what happens technically when you send money.

Imagine this scenario:

You open your UPI app and send ₹500 to a shopkeeper.

The entire process feels instant.

But behind the scenes, multiple systems are communicating incredibly fast.

Step 1: You Open the UPI App

Apps like:

- Google Pay

- PhonePe

- Paytm

- banking apps

Act as interfaces between users and banking infrastructure.

The app itself does not directly “hold” your money.

Your bank does.

The app mainly acts as

- communication layer

- authentication interface

- transaction initiator

Step 2: You Enter Payment Details

You:

- scan QR

- enter amount

- choose bank account

Then confirm payment.

This starts the transaction request.

Step 3: Authentication Happens

Before money moves, the system verifies:

- who you are

- whether you authorized the payment

Usually using:

- UPI PIN

- device verification

- app authentication

Security is critical because real bank accounts are involved.

Why UPI PIN Matters So Much

One important thing many users misunderstand:

UPI PIN is not just an app password.

It’s a banking authorization mechanism.

That’s why:

- sharing UPI PIN is dangerous

- fraud scams target PIN access

Without successful authentication, the transaction cannot proceed.

Step 4: The App Talks to Your Bank

Once authenticated, the app sends a request to your bank.

Your bank checks:

- account balance

- account status

- transaction validity

If everything looks correct, the bank prepares approval.

Step 5: NPCI Enters the Picture

This is where the system becomes really interesting.

NPCI acts like the central switching infrastructure.

Think of it like a massive digital traffic controller for payments.

It routes requests between:

- sender bank

- receiver bank

Extremely fast.

The Hidden Infrastructure Behind UPI

Most users never see this layer.

But behind every payment exists the following:

- APIs

- secure banking servers

- transaction routing systems

- verification layers

- encrypted communication channels

All operating within seconds.

Step 6: Receiver Bank Gets the Request

NPCI forwards the transaction to the receiver’s bank.

That bank verifies:

- receiver account exists

- account can accept payment

- transaction details are valid

If successful:

The receiving bank approves the credit.

Step 7: Transaction Confirmation Happens

Once both banks approve:

- sender account gets debited

- receiver account gets credited

Then:

- success notification appears

- transaction ID gets generated

- payment history updates

All within seconds.

That speed is what makes UPI feel magical.

Why UPI Feels Instant

Technically, UPI involves multiple systems communicating:

- apps

- APIs

- banks

- NPCI infrastructure

- verification systems

Yet it often completes in under a few seconds.

That’s impressive engineering at national scale.

UPI Is Basically a Massive API Ecosystem

Underneath the user interface, UPI depends heavily on APIs.

Banks constantly exchange:

- transaction requests

- account validations

- authentication responses

- payment confirmations

Modern digital banking increasingly functions as interconnected software systems.

Why UPI Became So Popular in India

Technology alone doesn’t guarantee adoption.

UPI succeeded because multiple conditions aligned perfectly.

1. Smartphones Became Affordable

As smartphones spread across India:

digital payment accessibility exploded.

People suddenly carried internet-connected banking devices in their pockets.

2. Mobile Internet Became Cheaper

Affordable mobile data dramatically accelerated:

- app usage

- digital payments

- fintech growth

Without widespread internet access, UPI would not scale this quickly.

3. QR Payments Were Extremely Simple

No complicated setup.

No card machine required.

Even tiny businesses could accept digital payments instantly.

That lowered entry barriers dramatically.

4. UPI Reduced Friction

The easier something becomes:

the more people use it.

UPI removed:

- complexity

- delays

- unnecessary banking friction

And adoption exploded.

How Secure Is UPI?

This is one of the most important questions.

Because convenience without security becomes dangerous.

UPI systems use:

- encryption

- PIN authentication

- secure APIs

- device verification

- banking-level protection

But no system is completely risk-free.

The Biggest Security Problem Isn’t Technology

It’s social engineering.

Scammers often trick users into:

- sharing OTPs

- revealing PINs

- approving fraudulent requests

This is why awareness matters as much as infrastructure.

Common UPI Scam Techniques

Fraudsters commonly use:

- fake payment screenshots

- payment request scams

- customer care fraud

- QR manipulation

- phishing links

Interestingly, many scams exploit human behavior more than technical vulnerabilities.

Why Failed UPI Transactions Happen

Sometimes payments fail because:

- banks are overloaded

- servers are slow

- connectivity issues occur

- verification times out

Remember:

multiple systems must synchronize correctly.

At national scale, occasional failures are inevitable.

UPI Changed Small Businesses Forever

One of the most powerful effects of UPI was democratization.

Small vendors suddenly gained access to:

- digital payments

- transaction history

- cashless business models

Without expensive infrastructure.

This transformed local commerce.

India Became a Global Fintech Example

UPI attracted international attention because of:

- scale

- speed

- adoption

- simplicity

Many countries began studying India’s payment infrastructure model.

Because building instant payment systems at this scale is extremely difficult.

UPI Is Still Evolving

UPI is not finished evolving.

Modern developments include:

- credit integration

- international UPI support

- offline payments

- wearable payments

- AI fraud detection

The system continues expanding rapidly.

The Future of UPI

The next phase of UPI may include:

- voice-based payments

- AI-powered fraud prevention

- deeper fintech integration

- cross-border payments

- smart-device payments

Digital payments may increasingly become invisible background infrastructure.

What Makes UPI Technically Impressive

UPI succeeded because it balanced:

- simplicity for users

- complexity behind the scenes

That balance is hard.

Really hard.

Most users never think about:

- banking APIs

- transaction switching

- encrypted communication

- real-time verification

Because the experience feels effortless.

And honestly?

That’s great engineering.

Final Thoughts

UPI is more than just a payment system.

It represents:

- modern infrastructure

- fintech innovation

- API-driven banking

- digital accessibility

It quietly transformed how millions of people interact with money every single day.

The most interesting part is that users rarely think about the technology itself.

They simply expect instant payments now.

And that expectation alone shows how deeply UPI changed digital life in India.